By Nicola McDougall, Editor, The Female Investor

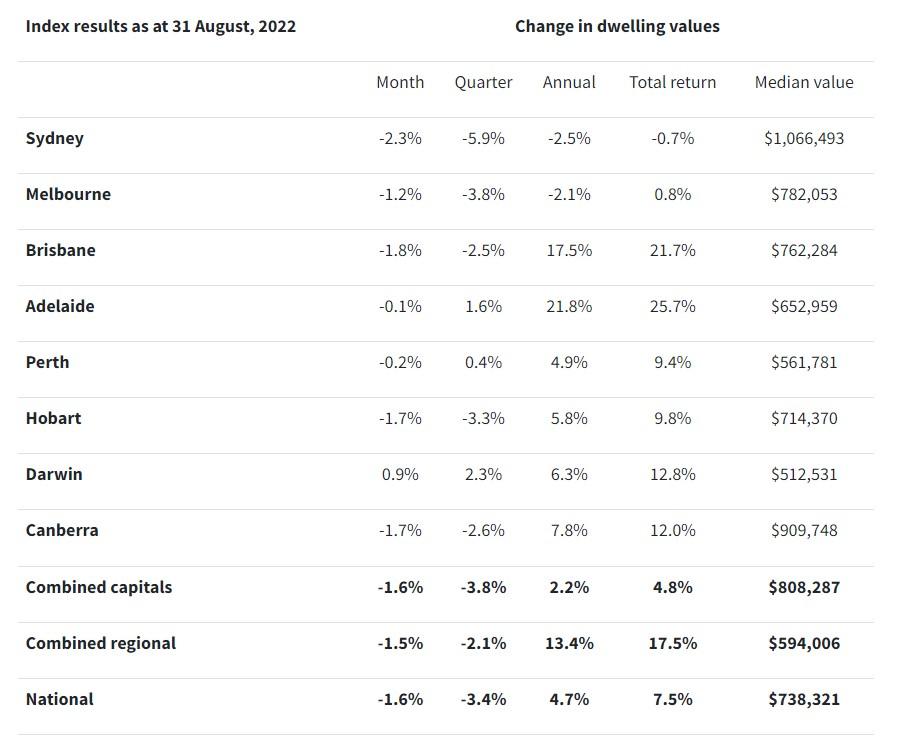

CoreLogic’s national Home Value Index (HVI) recorded a fourth consecutive month of decline in August, with the downturn accelerating and becoming more geographically broad-based. Down -1.6% over the month, the national index recorded the largest month-on-month decline since 1983.

Every capital city apart from Darwin is now in a housing downturn, with a similar scenario playing out across the rest-of-state regions, where only regional South Australia recorded an increase in housing values for the month.

Sydney continued to the lead the downswing, with values falling -2.3% over the month, however weaker conditions in Brisbane accelerated sharply through August, with values falling -1.8%.

CoreLogic’s research director, Tim Lawless, said Brisbane’s shift into decline had been acute after almost two years of sustained growth due to record high internal migration and relative affordability.

“It was only two months ago that the Brisbane housing market peaked after recording a 42.7% boom in values. Over the past two months, the market has reversed sharply with values down -1.8% in August after a -0.8% drop in July,” Mr Lawless said.

After recording significantly stronger appreciation through the upswing, the fall in regional dwelling values is catching up with the capital cities. Regional home values were down -1.5% in August compared with a -1.6% fall in values across the combined capitals. Between March 2020 and January 2022 regional dwelling values surged more than 40% compared with a 25.5% rise for the combined capitals.

“The largest falls in regional home values are emanating from the commutable lifestyle hubs where housing values had surged prior to the recent rate hikes,” Mr Lawless said. “Over the past three months, values are down -8.0% across the Richmond-Tweed, -4.8% across the Southern Highlands-Shoalhaven market and -4.5% across Queensland’s Sunshine Coast. “

Across the 41 regional SA4 sub-regions analysed, only seven areas recorded a rise in housing values in August including the northern suburbs of Adelaide (0.9%), Perth’s North East and Mandurah (0.6% / 0.5%) and the Coffs Harbour-Grafton region (0.6%).

The annual trend in housing values is rapidly levelling out. After moving through a peak annual growth rate of 21.3% in November last year, the annual growth rate across the combined capitals has eased back to just 2.2%. Values across Sydney (-2.5%) and Melbourne (-2.1%) are now below the level recorded this time last year.

Despite the recent weakness, housing values across most regions remain well above pre-COVID levels. Home values in all capital cities and rest-of-state regions, bar Melbourne, remain 15% or above the levels recorded in March 2020, implying most home owners have a significant equity buffer before their home is likely to be worth less than what they paid.

“A 15% peak to trough decline would roughly take CoreLogic’s combined capitals index back to March 2021 levels,” Mr Lawless said. “Additionally, many home owners would have had at least a 10% deposit and paid down a portion of their principal, the risk of widespread negative equity remains low.”

Mr Lawless expects the downturn will continue to play out through the remainder of the year, and possibly into 2023.

“It’s hard to see housing prices stabilising until interest rates find a ceiling and consumer sentiment starts to improve,” he said.

“From current levels, interest rates are likely to increase by at least another 75 basis points and there is a good chance advertised stock levels will accumulate through the spring selling season, providing more choice for buyers and adding further downwards pressure on housing values.”

The trend in freshly advertised housing stock being added to the capital city markets was 13.4% higher than a year ago and 6.5% above the previous five-year average over the four weeks ending 28 August.

“Despite the downwards trend in new listings through the colder months, the total number of capital city homes advertised for sale held reasonably firm, and there are currently 11.3% more homes available for sale compared to this time last year,” Mr Lawless said.

“Sydney and Melbourne, where the housing downturn is more advanced, are already seeing total advertised stock rise to above average levels and there is a good chance the other capitals will follow suit as listings rise through spring and demand continues to taper.”

Higher advertised stock levels are mostly the result of less housing demand rather than a rise in the number of new listings being added to the market. Nationally, CoreLogic estimates the number of home sales over the three months to August was -14.8% below the same period a year ago, but larger declines were evident across some cities including Sydney (-35.4%), Canberra (-18.9%) and Melbourne (-16.5%).

“Between winter and spring we typically see a 22% rise in the number of new capital city listings based on the pre-COVID five-year average. The flow of new listings this spring season may not be quite as active with the housing downturn dissuading some prospective vendors, but we are likely to see more listings added to the market than in winter,” Mr Lawless said.

“At the same time we are expecting to see less buying activity as higher interest rates and low sentiment continue to weigh on demand. Should this scenario play out, the net result will be an accumulation of advertised supply that could further weigh down values.”

Rental rates increased a further 0.8% in August across CoreLogic’s national rental index, easing after the monthly trend peaked in May when rents rose by 1.0%. The slowdown in rental appreciation comes after annual rental growth reached double digits (10.0%) for the first time since at least 2006 when CoreLogic rental statistics commence.

The slowdown was most evident across regional Australia, where the annual rate of rental growth eased from 12.5% in November last year to 10.1% over the 12 months ending August. Growth in capital city rental trends look to be easing a little as well, with the combined capitals recording a 10.0% rent rise over the past year, while the monthly trend eases from a recent peak of 1.1% in May to 1.0% in August.

The slowdown in rental growth is more apparent in the detached housing sector, where renting tends to be more expensive. House rents across the combined capitals have increased at more than double the pace of unit rents over the past five years, rising 21.8% and 10.8% respectively.

“This trend is reversing as tenants become more willing to rent in higher density situations, especially in Sydney and Melbourne where unit rents are now rising at a much faster pace than house rents,” Mr Lawless said. “Potentially we are seeing the first signs of smaller rental households that formed earlier in the pandemic reverting back to larger households or utilising higher density rental options to combat worsening rental affordability.”

National housing completions are also likely trending higher in 2022, particularly in the detached house segment, as an inflated number of builds slowly work through the construction pipeline. Mr Lawless said the trend may relieve some pressure on rental demand, as some tenants move out of rentals into their new homes.

However, as overseas migration normalises, it is likely rental demand will increase further. Without any signs of a material rise in rental supply, the outlook for rents remains one of further growth.

With rents consistently rising while housing values broadly trend lower, gross rental yields are firmly in recovery mode. After capital city gross dwelling yields bottomed out at the record low of 2.96% in February this year, yields have consistently risen to reach 3.29% in August.

While capital city yields are still well below the pre-COVID decade average (4.0%), considering the outlook for lower housing values and higher rents, we could see rental yields returning to around average levels over the next year.

The outlook for the housing market remains intertwined with the trajectory of interest rates. Forecasts for the terminal cash rate generally range from the mid-2% to the mid-3% range, although financial markets are pricing in a peak cash rate of just over 4% by August next year. Mr Lawless said the range of forecasts for the cash rate highlights the sheer uncertainty associated with inflation, wages growth and monetary policy.

“As borrowing power is eroded by higher interest rates and rising household expenses due to inflation, it’s reasonable to expect a further decline in consumer confidence and lower housing demand,” Mr Lawless said.

The silver lining to lower housing prices is an improvement in some measures of housing affordability. As outlined in the recently released June quarter ANZ CoreLogic Housing Affordability report, decreasing housing values saw the time needed to save a 20% deposit fall for the first time in almost two years across the capital cities, while the dwelling value to income ratio also declined. As housing values trend lower and incomes rise, we expect to see a further reduction in these barriers to entering the housing market.

However, mortgage costs and rents are rising, and household budgets are stretched. The portion of annual household income required to service a new mortgage nationally increased to 44.0% in June, up from 40.4% over the March 2022 quarter, likely offsetting some of the improvements in other measures of housing affordability.

“The wash up is that lower housing prices and higher incomes should make home ownership more achievable for non-home owners, but headwinds remain in being able to save for a deposit and demonstrate the ability to service a loan amid such a high cost of living,” Mr Lawless said.

“With spring upon us, advertised stock levels are expected to rise. Inventory was already higher than average across some markets at the end of winter (Sydney/Melbourne/Hobart) and, although the flow of new listings may not be as high as previous years, we could see advertised supply accumulating through spring due to a lack of housing demand.

“Amid higher advertised stock levels, vendors will be competing across a larger pool of available supply for fewer buyers. While this is positive news for buyers, sellers will need to be realistic in their pricing expectations and ensure they have a quality marketing campaign in place,” Mr Lawless said.

With labour markets so tight (the unemployment rate was 3.4% in July) and some momentum gathering in income growth, we are not likely to see a material increase in the number of distressed listings or forced sales, despite the higher interest rate environment. While labour markets could loosen to some extent under a contractionary interest rate setting, a substantial rise in unemployment or under employment seems an unlikely outcome.

The risk of housing stress is further minimised by serviceability buffers applied to borrowers as part of the loan approval assessment. Since October last year, borrowers were required to demonstrate an ability to repay their debt under a mortgage rate scenario with interest rate three percentage points higher than the current rate (2.5 percentage points prior to October 2021).

The recent upswing is important context in the current downturn. Although housing values are on track to record a significant drop, the risk of widespread negative equity remains low, considering the substantial rise in housing values between September 2020 and April 2022. Nationally home values rose by 28.6%; so even a 20% decline in housing values would result in housing values remaining above their pre-COVID levels.

Download a full copy of the Home Value Index for charts, graphs and Top 10 Capital city SA3’s with highest 12 month value growth.